Aim Higher Than "Not Running Out of Money"

(~READ TIME: 5 MIN)

The problem with traditional retirement planning is that its analysis is static and does not allow for adjustment based on what’s actually happened. This limiting issue is the reason the goal of traditional retirement planning has always focused simply on not running out of money. To accomplish this goal, traditional retirement planning seeks to find an individual’s “safe withdrawal rate.” A safe withdrawal rate is the highest withdrawal rate an individual can sustain that could pass all possible investment market scenarios within the research’s scope. In other words, how much can I take from my portfolio every year (with an inflation adjustment) without risking running out of money? This is why the outcome of traditional retirement planning is always stated as a probability of success or failure. (See our Insight entitled “Retirement Can’t Be Pass or Fail” for more)

Traditional Retirement Planning Focuses Only on Downside Risk

While this may sound desirable at first glance, this approach is way too conservative. It will leave far too much money on the table upon passing that could have been used to increase your quality of life during retirement should your actual investment market scenario end up better than the very worst that history could turn up. Traditional retirement planning only cares about the worst possible outcomes and ignores all the better (and mathematically more probable) outcomes. It has to do so because the approach taken in traditional retirement planning cannot adjust and incorporate reality. This approach has no choice but to assume and protect against the worst.

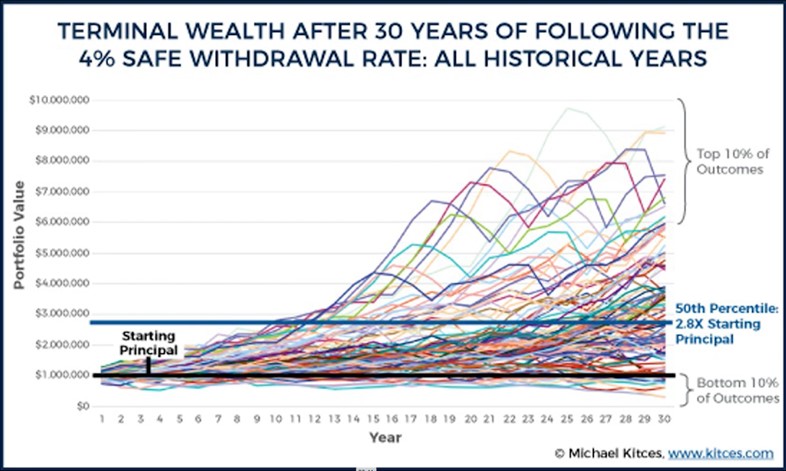

Don't Leave So Much Money on the Table

Michael Kitces, MSFS, MTAX, CFP, CLU, ChFC (www.kitces.com) produced this wonderful chart based on his research that illuminates just how much could be left on the table following a hypothetical 4% safe withdrawal rate “rule of thumb”:

In this example, a person begins with $1,000,000 and plans for a 30-year retirement. This person’s beginning withdrawal would only be $40,000 (4% x $1,000,000). Experiencing anything better than one of the bottom 10% of Monte-Carlo modeled investment market scenarios would leave this person with more money than when they started. Further, you can see the 50th percentile (or median) modeled observation would leave this person with 2.8x what they had when they started (or $2,800,000). Unfortunately, and all too often, this person might not have taken that vacation to Europe, helped a loved one, donated to a charity, bought that RV, or picked up that restaurant check when in fact, they could have all along. The only person that wins here is the traditional financial advisor, who charges based on the size of your portfolio that may actually continue to grow. This conflict of interest, along with lack of knowledge or initiative (aka "fat, dumb, and happy"), is why the retirement planning industry has failed to evolve even though time-tested research and principles have long existed to be able to do so. (See our Insight entitled “Why a Flat-Fee Advisor is Best for Retirees” for more)

Maintain Maximum Quality of Life During Your Retirement

Rather than looking for your safe withdrawal rate, we should look for your optimal withdrawal rate. Your optimal withdrawal rate aims to maximize your level of spending (i.e., quality of life, however you choose to spend/gift) while living during retirement and is dependent on many factors, including:

- Income (including Social Security claiming strategy)

- Assets (both financial and non-financial)

- Risk profile

- Asset allocation

- Portfolio construction and cost

- Level of tax planning

- Willingness and ability to be flexible in level of spending

- Level of risk management employed

Your optimal withdrawal rate will and should adjust as reality is incorporated as you progress down the path of what could be a 30-plus-year retirement. Finding and maintaining your optimal withdrawal rate is one of the key objectives of our “reality-based” approach to retirement planning. While we go to great lengths to manage the downside risks (i.e., bottom 10% of modeled investment market scenarios), we also take great care and pride in helping you make the most of the other 90% of better possible scenarios. Being a flat-fee, fiduciary advisor, our only interest is in seeing our clients make the very most of their retirement every step of the way. The primary way we achieve this goal is through the use of dynamic withdrawal rules and ongoing monitoring. (See our Insight entitled "Quantifying the Value of Dynamic Withdrawal Rules" for more)

If you would like help finding your optimal withdrawal rate, we stand by ready to help. To learn more, you can schedule a friendly, informal call for a date and time that is convenient for you here at this link: https://calendly.com/thrive-retirement-advisory-team or contact us here at any time.