Retirement Tax Planning Tips to Avoid Paying More Than Your "Fair Share" of Taxes

KEY TAKEAWAYS:

- Despite being a powerful lever to drive retirement success, many retirees don’t have a well-thought-out tax plan.

- A lack of planning for a handful of retirement milestones often leads to larger-than-needed (and expected) lifetime tax bills.

- Simple strategies exist to ensure retirees pay their “fair share” of taxes and nothing more.

As retirement planning specialists, we often see that many people approaching retirement believe that their taxes will decline during retirement. After all, our taxes increase along with our earnings throughout our working years, typically peaking late-career leading up to retirement. So, the opposite must hold: our taxes will decrease when our employment earnings stop. Right?? Not exactly!

Unfortunately, this misconception can lead retirees to approach retirement tax planning with less urgency than they would if they recognized how their inaction would result in more of their hard-earned savings being taken by Uncle Sam.

So here we share a few retirement tax planning tips to help you pay exactly what you owe and nothing more.

Culprits of A Higher Lifetime Tax Bill

While some people will pay lower taxes throughout retirement than during their working years, we often see the opposite with our clients – taxes will likely increase. This may be surprising since many retirees (and their advisors) underestimate the retirement income they can generate from their financial resources, like investments and Social Security benefits.

On top of that, it’s easy to overlook how all the years of diligent savings and investment growth in tax-deferred retirement accounts, like 401(k)s and IRAs, have created a big tax obligation that must eventually be paid. Here’s an example of how things may play out from a tax perspective.

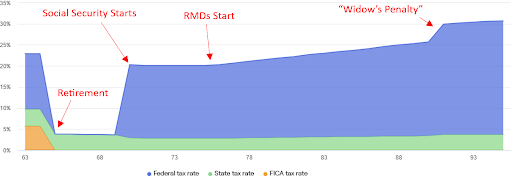

Figure 1. The effective tax rate for a married couple retiring at age 65 with $3M of investment assets ($2.25M in traditional IRAs and $750k in a taxable brokerage account). 4.25% flat state tax (MI).

As we would expect, there’s a dramatic decrease in this couple's taxes in the years immediately following retirement. This is due to following the “conventional” rule of thumb that says withdrawing from taxable accounts first (e.g., joint brokerage), followed by tax-deferred (e.g., traditional IRAs), then tax-free (e.g., Roth IRAs) is best. Although this approach provides an alluring respite from taxes in early retirement, it’s short-sighted and often results in larger-than-needed lifetime tax bills.

Retirement Tax Spike Caused by RMDs

Our example shows that taxes are creeping upward for most of this couple’s retirement after the spike caused by their Social Security income, eventually surpassing where they were before retiring. A big culprit is their required minimum distributions (RMDs) from retirement accounts, which are taxed as ordinary income, like wages. Because this couple opted to follow the rule of thumb of withdrawing from their taxable account first, their IRAs' balances (and embedded tax obligation) continued to grow.

Although investment growth is good, the fact that the IRS requires them to withdraw a larger proportion of their IRAs each year starting at age 75 -- even if they don’t need the extra income -- their income and taxes continue to rise. This problem then compounds because the IRS requires increasingly larger withdrawals as you age. The required minimum distribution percentage starts around 4% at age 75 and climbs to over 8% by age 90. All of these withdrawals are taxed as ordinary income, which is why it’s so important to be strategic about your retirement tax planning well before you start taking withdrawals.

For those with a spouse, the “widow’s penalty” is the cherry on top of these unexpected tax consequences, which we will discuss next.

The Widow’s Penalty

It’s hard to imagine anything more difficult than losing a spouse and companion. And if the emotional toll isn’t hard enough, financial consequences can worsen the situation for the surviving spouse. In this case, the “widow’s penalty.”

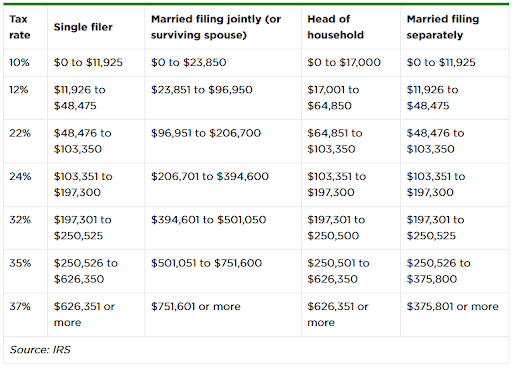

Tax rates are higher for singles than for married couples filing joint tax returns. The federal tax brackets 2025 table below shows that a couple with $200k of taxable income is in the 22% federal marginal tax bracket, whereas a single filer is in the 32% tax bracket – a 10% increase!

This is worth our attention because if one spouse died in 2025, the surviving spouse would file a joint tax return for 2025 and switch to filing as single in 2026. For example, if a couple’s only income were $200k from traditional IRA withdrawals (i.e., ordinary income), the tax bill would increase from ~$34k when filing jointly to ~$41k when the surviving spouse files as single -- a $7k difference. That’s a ~21% increase in taxes despite the surviving spouse’s income remaining the same, hence the widow’s penalty.

It’s important to mention that the above example doesn’t consider the standard deduction which was recently updated under the One Big Beautiful Bill Act. But if we take things one step further and factor in the surviving spouse losing half of their standard deduction ($31,500 for joint and $15,750 for single filers ages 65+) starting in the year they file taxes as a single taxpayer, their tax bill increases from ~$26k to ~$37k. That’s ~42% more taxes!

Admittedly, this is a simplified example that doesn’t consider other factors like state and Medicare taxes that can further penalize a surviving spouse. Many variables affect the magnitude of the widow’s penalty, such as the reduction or stoppage of Social Security and pension benefits and whether the deceased spouse had already begun taking required minimum distributions from their retirement accounts.

The takeaway is that it’s essential to be aware of the financial implications that come with the death of a spouse and take steps to mitigate the risks they pose to your retirement.

Social Security and Taxes

Social Security benefits have long been subject to federal taxation, with up to 85% taxed once your income crossed modest thresholds—$25,000 for single filers or $32,000 for couples—levels that were never adjusted for inflation.

As a result, about 65% of retirees were paying taxes on their Social Security benefits as of 2024. The new One Big Beautiful Bill Act (OBBB) changed this landscape by adding an enhanced deduction for older Americans: $6,000 for individuals age 65+ and $12,000 for married couples (both 65+).

This deduction phases out above $75,000 AGI for singles and $150,000 for couples, effectively shielding most lower- and middle-income retirees from paying federal income tax on their benefits. The relief is temporary, applying through 2028, which means retirees should review income strategies—such as Roth conversions, withdrawal sequencing, and charitable distributions—during this window to maximize the advantage.

Pay Your Fair Share (But No More)

Simple retirement tax planning strategies can help you avoid unnecessarily high taxes throughout your lifetime. Often, by simply developing a retirement plan that considers the sources and timing of withdrawals to create your retirement paycheck and pairing it with Roth IRA conversions, you can limit your tax bill to paying your fair share and nothing more.

If you are ready to forgo rules of thumb intended for the masses in favor of a tax plan customized to your unique circumstances, we are here to help. Click here to get your complementary Thrive assessment and schedule an informal, introductory call with one of our retirement planning specialists to get started.