How to Apply Dynamic Withdrawal Rules to Optimize Your Retirement Withdrawal Strategy

KEY TAKEAWAYS:

- Dynamic withdrawal rules let retirees start with higher withdrawal rates while maintaining flexibility to cut back during downturns.

- Establishing spending floors, boundaries, and adjustment rules can materially improve retirement success rates.

- Since most general financial planning tools cannot model dynamic rules effectively, it may be helpful to work with a retirement planning specialist.

As retirement planning specialists, we always seek to find ways to create opportunities for retirees to enjoy more from their savings while protecting against risks that could derail their plans. In past Insights, we have written on the tremendous value dynamic withdrawal rules can bring to a retirement plan through the strategy’s ability to manage sequence of returns risk (see our Insight entitled “Dynamic Withdrawal Rules – The Greatest Opportunity for Retirement Plan Optimization” for more).

We have also written about how dynamic withdrawal rules can allow a retiree to start with a higher initial withdrawal rate while actually lowering the retiree’s risk at the same time (see our Insight entitled “Dynamic Withdrawal Rules – Higher Withdrawals With Less Risk” for more).

In this Insight, we focus on the practical side—how we determine the right set of dynamic withdrawal rules and apply them to real retirement plans. (If you’d like one of our retirement planning specialists to apply these rules to your retirement plan, you can schedule a complimentary call here.)

How to Determine Appropriate Dynamic Withdrawal Rules

We need to take several steps before determining an appropriate set of dynamic withdrawal rules. We start by analyzing your retirement spending plan, testing whether your assets can sustain your desired lifestyle, and then layering in rules that provide both flexibility and protection. Each step helps ensure your withdrawals are realistic, resilient, and aligned with your long-term goals.

1). Analyze Your Retirement Spending Plan

We start by looking at a client’s retirement spending plan (see our Insight entitled “How to Create a Retirement Spending Plan” for more). We want to notice bottom-line spending needs and the breakdown of the desired spending between essential expenses, discretionary expenses, and desired legacy objectives.

For example, say we have a couple with a bottom-line after-tax spending desire of $180,000 per year. Further, the $180,000 is broken down into $148,000 for essential expenses, $22,000 for discretionary expenses, and $10,000 for desired legacy giving.

This is one of the reasons it’s so important to think carefully about your retirement spending goals in advance—clarity on what you truly need versus what would simply be nice to have becomes the foundation for setting rules that can adapt over time.

2). Test That Assets Can Support Bottom-Line Spending

Now that we know the couple’s desired retirement spending level, we can test that their assets are sufficient to sustain the desired level of spending through their retirement time-horizon while investing market-based assets at an appropriate asset allocation (see our Insight entitled “How to Determine a Proper Asset Allocation for Retirement” for more).

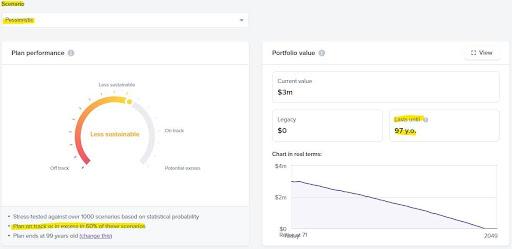

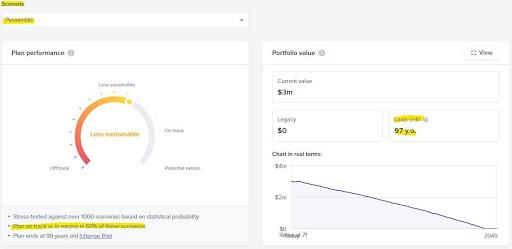

We test using Monte Carlo simulation analysis and historical simulation analysis, as both methods have their pros and cons. Building off our earlier example, say this couple has $3,000,000 of investment assets invested in a 50% stock and 50% bond portfolio and is receiving $65,000 annually from Social Security. Our Monte Carlo testing, seen below, shows this couple would have only a 60% chance of sustaining their $180,000 desired level of spending, assuming no changes were made but an annual adjustment for inflation. Further, at the 30th percentile of simulated observations (i.e., a pessimistic scenario), the couple would run out of money two years short of their 99-year-old life expectancy based on current Social Security mortality tables.

3). Calculate Initial Withdrawal Rate

This couple wants to be able to spend $180,000 per year on an after-tax basis. In this case, they need to raise enough from the portfolio to cover what’s left after considering federal and state income taxes and their proceeds from Social Security [the math: desired after-tax spending + tax liability – Social Security = amount needed from the portfolio]. The couple in this example must be able to raise $150,000 from their $3,000,000 portfolio, leaving the couple with a 5.0% initial withdrawal rate.

4). Assess Spending Flexibility and Spending Floor

A 5.0% initial withdrawal rate seems to be too high for this couple, given the 60% Monte Carlo probability of success. Fortunately, this couple is comfortable considering dynamic withdrawal rules as they have some flexibility in their retirement spending plan. The couple in this example is willing to cut back on their $22,000 of discretionary spending and $10,000 of legacy giving if needed for a period of time. After considering this level of spending flexibility, the couple is left with a spending floor of $148,000 ($180,000-$32,000) to meet essential living expenses.

5). Add a Set of Dynamic Spending Rules and Test for Effect

Given that our initial withdrawal rate is 5.0%, we can enter our spending floor and start by creating boundary rules at 4.0% and 6.0%. Further, if those boundaries are crossed, we will either increase portfolio withdrawals by 10% or decrease portfolio withdrawals by 10%, respectively. In summary, following are the rules that are set after testing and determining they were appropriate for this example couple as well as the practicable interpretation of the rules:

- Beginning Portfolio Value = $3,000,000

- Desired After-Tax Spending = $180,000

- Floor After-Tax Spending = $148,000

- Initial Withdrawal Rate = 5.0% (after tax and Social Security, need $150k from portfolio)

- Upper Boundary Rule = 6.0% [portfolio withdrawals decrease by $15,000 (10% of current $150k)]

- Lower Boundary Rule = 4.0% [portfolio withdrawals increase by $15,000 (10% of current $150k)]

RULES INTERPRETATION:

IF PORTFOLIO VALUE DECREASES BELOW $2,500,000 (-17%), SPENDING DECREASES TO ~$165,000 (UPPER 6% BOUNDARY)

IF PORTFOLIO VALUE INCREASES ABOVE $3,750,000 (+25%), SPENDING CAN INCREASE TO ~$195,000 (LOWER 4% BOUNDARY)

The results of these rules work for the couple bringing their probability of success up to an acceptable 85% as can be seen below:

6). Monitor and Reset Rules if Boundary Breached

Rules should be monitored and reviewed at least semi-annually. If a boundary is passed and the spending level changed, the rules should be reset to reflect the new portfolio and spending levels.

Dynamic Withdrawal Rules Are Not Magic

How is it that just adding a set of dynamic withdrawal rules can have such a positive impact on retirement plan outcomes? It is not magic. Dynamic withdrawal rules allow you to start with a higher withdrawal rate because of a willingness to adjust spending downward should we happen to experience one of the pessimistic scenarios for which we plan.

In retirement planning, it is necessary to plan based on pessimistic scenarios because the risk of running out of money is far more serious than the risk of passing away not having spent everything. While we plan for 10th and 20th percentile pessimistic scenarios that can happen, they are not representative of the median expectation. So while the extreme pessimistic scenarios are possible, and dynamic withdrawal rules are prepared to lower your spending in response should they happen, these extreme downside scenarios are not probable.

As long as you are willing to adjust your spending downward should you be required to do so, you can start with a higher withdrawal rate and hopefully increase that withdrawal rate over time if you experience anything but the most pessimistic of scenarios.

Who Can Help Me Determine and Implement the Best Retirement Withdrawal Rules for My Situation

Understanding how dynamic withdrawal rules work is one thing—implementing them effectively in your retirement withdrawal strategy is another. And while the rules themselves are not magic, applying them correctly does require careful analysis, the right tools, and ongoing monitoring.

The two predominant software systems most generalist financial advisors utilize (i.e., Money Guide Pro or eMoney) cannot model these dynamic withdrawal rules. Fortunately, any good retirement specialist (see our Insight entitled “Retirement Specialist or Financial Advisor” for more) should have access to one of the two retirement planning specialist software systems that can accommodate the modeling of dynamic withdrawal rules.

In fact, dynamic withdrawal rules are but one of the many tools a good retirement specialist should have at their disposal to help you optimize your retirement. In addition to having the tools, a good retirement specialist will also understand the pros and cons of specific tools and how they work or do not work together. This knowledge can help to fine-tune the optimization of your retirement plan even further.

For instance, as complicated as this process of setting and implementing dynamic withdrawal rules may seem, this example is actually quite simplified and does not take into consideration the effects of tax management and income optimization strategies (see our Insight entitled “10 Reasons Most Retirement Plans Are Overly Conservative” for more).

If you would like help determining your optimal dynamic withdrawal rules for retirement, our retirement planning specialists are happy to help. Get started now by scheduling your complimentary call and Thrive Assessment here.