Low-Hanging Fruit: How to Use Liquidity to Protect Yourself from Retirement Risks

KEY TAKEAWAYS:

- There's no silver bullet to protect retirees from risk – a multi-pronged approach is needed.

- Identifying quick wins that provide a big impact is the best starting point.

- Using a simple idea to integrate liquidity into your retirement income plan better can have an outsized effect on reducing your risk.

Liquidity: the efficiency or ease with which an asset or security can be converted into ready cash without affecting its market price.

Eating your fruits and vegetables is meaningless if you are a hermit whose definition of exercise is channel surfing. Building our body's resilience to better protect against everyday stressors requires paying attention to all aspects of our lives rather than relying on a silver bullet. A reasonable diet, exercise, and meaningful relationships better position us to thrive than fixating on eating like a rabbit.

As with your physical wellness, your financial wellness is best improved with a multi-pronged approach. And, when looking to improve any area of your life, it's smart to start with quick wins that provide a big impact. As retirement planning specialists, we often find that financial liquidity doesn't get the attention it deserves when it comes to retirement income planning.

But, as you will see here, using a simple idea to better integrate liquidity into your retirement income plan can have an outsized effect of protecting you from one of the five big retirement risks you face as a retiree.

Murphy's Law a.k.a. Sequence of Returns Risk

When a retiree starts to convert their investments (from a 401(k), IRA, brokerage account, etc.) into a retirement "paycheck," they are exposed to the risk of poor investment returns coinciding with their need to sell investments to generate income.

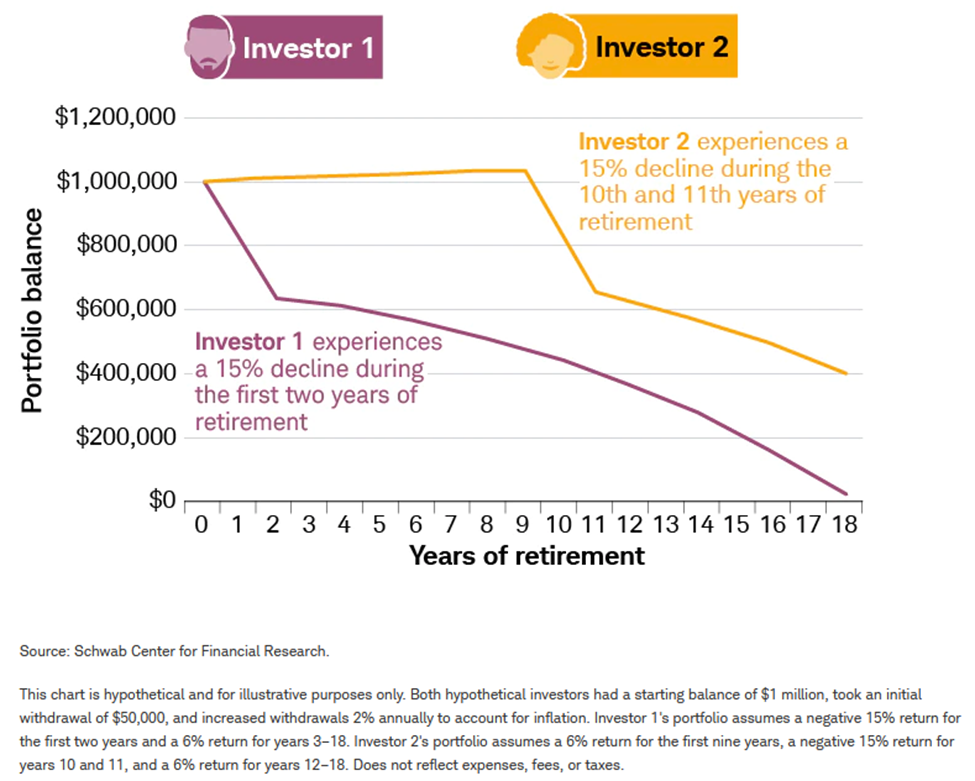

If you follow our writing, you are likely aware that negative investment returns are especially problematic during the Retirement Red Zone – the years immediately before and after retiring. This is because selling investments at reduced values compounds losses, which greatly impacts a portfolio's ability to recover and sustain a retiree's income needs over a 20+ year retirement. This phenomenon is known as "sequence of returns risk," and its ability to decimate the value of an investment portfolio can be seen in the chart below.

Timing of Retirement Withdrawals and Why It Matters

Two investors with an identical ~3.5% average return over the first 18 years of retirement.

Sequence of returns risk is a complex problem, which makes it tempting to jump to a complex solution. However, considering the "low-hanging fruit," it becomes clear that ample liquidity is a straightforward and potent first line of defense.

But while having cash available for a "rainy day" is necessary for contingencies, it isn't sufficient if you aim to build a resilient retirement income plan. For that, you must be more intentional by expanding your use of liquidity to fund near-term spending to protect against a poor sequence of returns, like those experienced by unlucky "Investor 1". So let’s take a look at some steps that would make sense when putting together your retirement red zone risk mitigation plan.

Estimate Your Retirement Income Needs

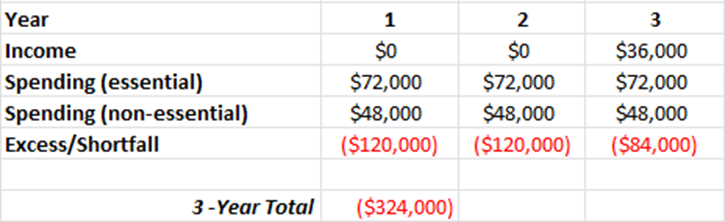

Let's assume that a soon-to-be retiree, Mary, estimates she will spend $120,000 annually (ignoring taxes and inflation for simplicity) over the first three years of retirement, and her only source of income (excluding her retirement savings) is $36,000 of Social Security starting in year three.

Mary's 3-Year Cash Flow Estimate

As we see, Mary has a $324,000 cash flow shortfall over the next three years that she will need to fund with withdrawals from her retirement savings. However, given the risk of a poor sequence of returns over that timeframe, relying solely on a mix of stocks and bonds with values that can change dramatically over short time horizons exposes her to unnecessary risk. She needs a different approach.

Establish An Income Floor

Pension funds and insurance companies wouldn't exist without harnessing the power of liquidity. They use "asset-liability matching," which is an approach that aims to match the timing of income from an asset sale with a future liability. As an example, a pension fund may buy a bond that matures (and returns its principal) in five years to provide the necessary income to cover their pension payment obligations in, you guessed it, five years. For a retiree like Mary, liabilities are her estimated spending needs, and assets are her savings (e.g., 401(k), IRA, brokerage account).

As retirement planning specialists who aim to help clients mitigate risks whenever possible, we use asset-liability matching to build a stable source of income to fund spending in early retirement when sequence of return risk is most harmful. This is called an "income floor" and typically funds spending for the first one to three years of retirement based on client preferences.

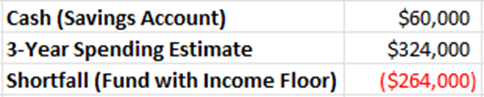

In Mary's case, she would determine how much of her retirement savings to allocate to her income floor by subtracting the $60,000 cash in her savings account from her 3-year cash flow shortfall.

As Mary builds her investment portfolio for retirement, she will use $264,000 for her income floor, which would be comprised of investments that return her principal (like Individual treasury bills, CDs, and bonds) on maturity dates that match the timing of her income needs. For example, she could buy $120,000 of treasury bills that mature in years one and two and $84,000 that mature in year three (known as "laddering") to match her spending estimates. The remaining portion of her portfolio would be invested in a mix of stocks and bonds to provide the necessary long-term growth to fund decades of retirement spending.

The beauty of this approach is its flexibility. Based on Mary's preferences, she could only fund her essential expenses with an income floor over the next three years, knowing that she has wiggle room to reduce non-essential spending if needed. If so, her income floor is reduced to $180,000, and any income for non-essential spending would come from selling investments in her stock and bond portfolio.

Consider HELOCs, Asset Credit Lines, and Reverse Mortgages If Needed

Once you have estimated your retirement income needs and established an income floor that matches assets to liabilities, you may still find that you need cash for additional unexpected expenses. In that case, it’s helpful to know that other forms of liquidity exist that should not be ignored.

It might surprise you to find that as retirement planning specialists, we are not opposed to our clients using debt when it makes financial sense to do so. We encourage most clients to obtain either a home equity line of credit (HELOC) or an asset credit line (secured by their brokerage account) since they help bolster liquidity and can be tapped quickly in a pinch.

While reverse mortgages can also be helpful, we are much more selective with their use, given their costs and complexity. Considering these tools as supplements to a retirement income plan is beneficial, like what a multivitamin is to nutritious foods.

Tying It All Together

Liquidity is a necessary piece of a resilient retirement income plan. When you pair an income floor with a diversified portfolio of stocks and bonds, you are better protected from sequence of returns risk while maintaining the inflation protection offered by long-term investment growth.

This approach complements our flexible spending plans, which form a multi-pronged approach to better protect you from risk. The result is increased confidence that you can weather potentially nasty investment markets.

If you are ready to see how adding liquidity can help your retirement income planning, schedule an informal call with a retirement specialist from our team to help you map out your retirement plan and get your complementary Thrive Assessment.