Social Security Claiming Strategies: How to Decide What’s Best for You

KEY TAKEWAYS:

- Social Security is often the only guaranteed, inflation-adjusted income stream in retirement, making the claiming decision foundational to your entire retirement income plan.

- For married couples, it’s important to coordinate claiming strategies to increase your chances of optimizing long-term outcomes.

- The “wait until 70” rule of thumb might not be the best fit for everyone, since health, income needs, liquidity, and overall financial strategy can materially change the optimal choice.

At some point in your retirement planning process, Social Security will no longer be an abstract government program, but a very personal decision. The age you claim Social Security affects all parts of your retirement plan—cash flow, inflation protection, survivor benefits, and even your broader tax strategy.

As retirement planning specialists, we know that the decision about when to start taking your Social Security benefits can be confusing. Here, we share some high level thoughts and considerations to help you think more clearly about optimal Social Security claiming and how it may apply to your unique situation.

Understanding Your Social Security Statement

First, it’s important to understand the different figures shown on your Social Security statement, since these numbers form the foundation of any claiming decision (you can access your most up to date Social Security statement by creating or logging into your account at ssa.gov).

Your Social Security statement outlines your estimated retirement benefit at age 62, at your Full Retirement Age, and at age 70, helping you clearly see the permanent impact of claiming early versus delaying.

Your Full Retirement Age (FRA) will be either 67, or somewhere between 66 and 67 if you were born before 1960. Your Full Retirement Age is important as it is the age at which you’re entitled to receive your full, unreduced Social Security retirement benefit based on your earnings record. This “full” amount is called your Primary Insurance Amount (PIA). This number serves as the baseline from which reductions and delayed retirement credits are calculated, and it is central to evaluating any claiming strategy.

The implications of your social security claiming strategy will thus stem from when you start claiming in relation to your full retirement age. Here are the implications of what happens if you start taking benefits before or after your FRA.

When Can You Start Taking Social Security Benefits?

You are eligible for Social Security benefits as early as age 62. And while that might sound appealing at first, the trade off is that your retirement benefit will be permanently reduced at any claiming age before your FRA.

If your FRA is 67 and you were to claim at age 62 (60 months early), you would be locking in a 30% discount to your FRA benefit:

- First 36 months: 36 × 0.5556% = 20%

- Next 24 months: 24 × 0.4167% = 10%

- Total reduction at 62: 30% (you receive about 70% of your FRA benefit)

This 30% reduction is permanent. Your annual Cost of Living Adjustment (COLA)(or inflation) adjustments and survivor benefits will forever be impaired.

Now, what happens if you wait and take your benefits later?

You can also receive Delayed Retirement Credits (DRCs) for every month that you delay claiming your retirement benefits beyond your FRA all the way up to age 70. If your FRA is 67 and you were to claim at age 70 (36 months delayed), you would be locking in a 24% increase to your FRA benefit:

- Delayed 36 months: 36 × 0.6667% = 24%

This 24% increase would also be permanent. And not only would your monthly check be higher, but your future cost of living adjustments and any survivor benefits would grow from that larger base as well.

Social Security is Foundational to a Retirement Income Plan

Your Social Security retirement benefit is a foundational piece to your retirement income plan. It is likely the only guaranteed inflation-adjusted income that you will receive. This is reliable, guaranteed income that you cannot outlive and this income is inflation adjusted to keep your purchasing power intact.

It is for this reason that conventional wisdom has been to wait until age 70 to claim your retirement benefit, so you can maximize this foundational stream of income. But that may not always be the best answer…

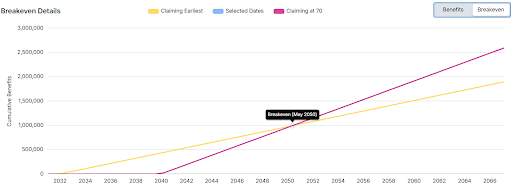

Let’s look at an example of Bill and Judy, who are eligible to claim at age 62 in 2032 or they could delay to age 70 in 2040:

Bill and Judy would receive the same amount of Social Security under either decision (i.e., breakeven) by May of 2050, at age 81. It would seem that Bill and Judy would be far better off waiting until age 70 to claim given their 97-year life expectancy. They would receive $698k more in lifetime benefit than the $1,897k they would receive if they claimed at 62.

If you’re working with a retirement planning specialist or a financial advisor, they may be able to input your specific estimates into a financial planning tool so you could see the break-even ages and total numbers that apply to your retirement plan.

The Problems with Social Security Claiming Strategies Based on Conventional Wisdom

As is always the case with “conventional wisdom” or rules of thumb, this singular overly simplified logic does not consider nuance, you, or your unique situation. The decision to wait until age 70 is not always so clear. Here are a few other factors you should consider in your Social Security claiming strategy.

Life Expectancy

Of course, none of us know what our life expectancy will be. But if you or your spouse have a known health issue and/or feel your odds of living past 81 are not great, it would likely not make sense to wait until age 70.

Income Needs

Claiming early could make sense if other ways to fund retirement spending would be more damaging. Not everyone has the choice to work longer or the financial resources and other retirement assets to “finance the gap.” You wouldn’t want to use debt, deplete cash for emergencies, or sell investments at an inopportune time to finance your current spending needs.

Lower Earner in a Married Couple

If one spouse has a much larger earnings record, it can be beneficial for the higher earner to delay (to boost the survivor benefit), while the lower earner claims earlier to bring money in sooner. This strategy can be beneficial, because in the event of either spouses’ death, only the highest benefit amount would remain.

You Were to Invest Your Benefit Amount

An interesting (and material) assumption used in the breakeven math between claiming ages is that it is assumed if someone claims early, that they are spending the Social Security retirement benefit. Because of this assumption, a 0% discount rate is used in the break-even analysis. In other words, the math assumes a dollar today is not worth more than a dollar in the future because it’s not invested.

But what if someone decided they could take their Social Security benefit and invest the proceeds instead of spending them? The long-term average real return (i.e., excluding inflation) on a 60% stock and 40% bond portfolio is 6.8%. Discounting the streams of income (to account for the opportunity cost of waiting and not investing) from both claiming strategies (62 and 70) by 6.8% shows that delaying until age 70 never surpasses claiming early at 62 and investing the proceeds:

As there are reasons to claim early, there are also many other reasons to wait until age 70. Many people are indeed served well by waiting to claim until age 70, especially those we come across that want to take advantage of Roth IRA conversion opportunities.

Our point is that the Social Security claiming decision is not as straight forward as the singular logic that conventional wisdom is predicated upon. As is always the case, critical thinking applied to one’s unique circumstance is always in the best interest of any one individual (or couple) trying to make an optimal Social Security claiming decision.

If you’d like guidance in deciding which Social Security claiming strategy would be most beneficial to your long-term plan, you can schedule a complimentary Thrive Assessment analysis with our retirement planning specialists here.